A Strategic Window to Lower Your Mortgage and Unlock Equity

Unlock Your Home’s Potential—And Possibly Secure a Rate Even Lower Than Today’s Market

Right now, the market is presenting a rare opportunity: borrowing costs have come down significantly, while homeowners are still holding strong equity. That combination creates real financial leverage—if you act on it.

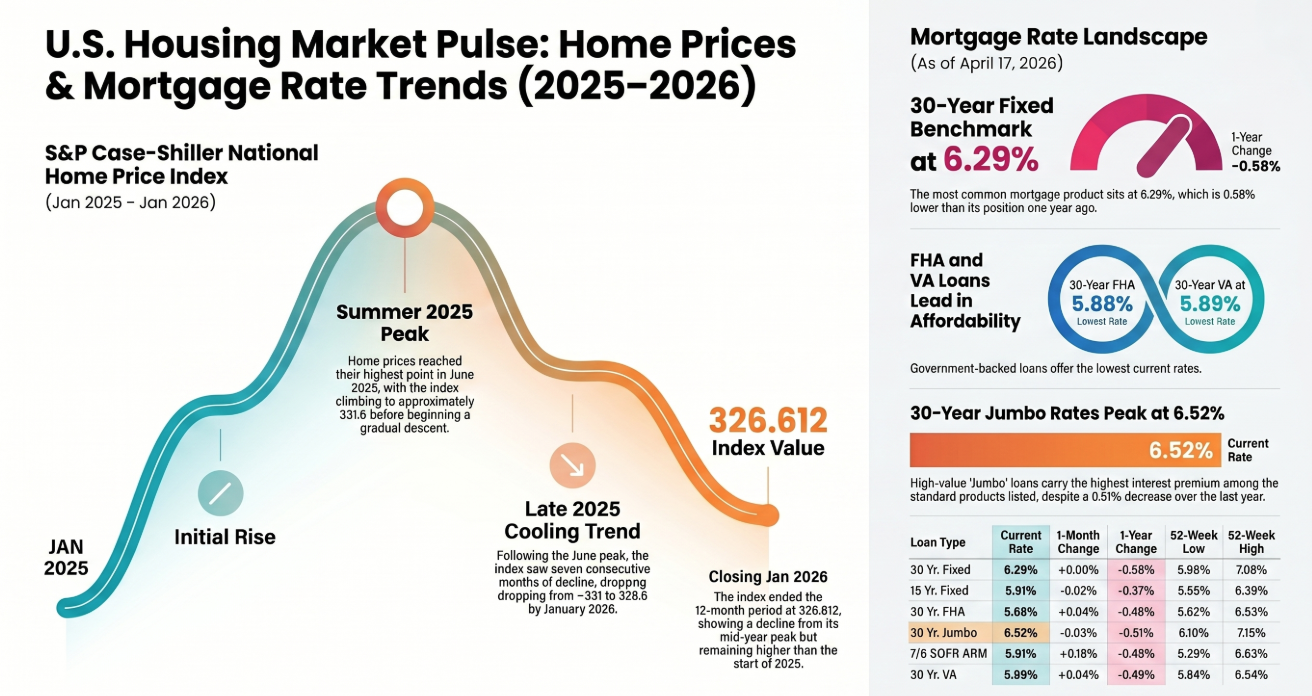

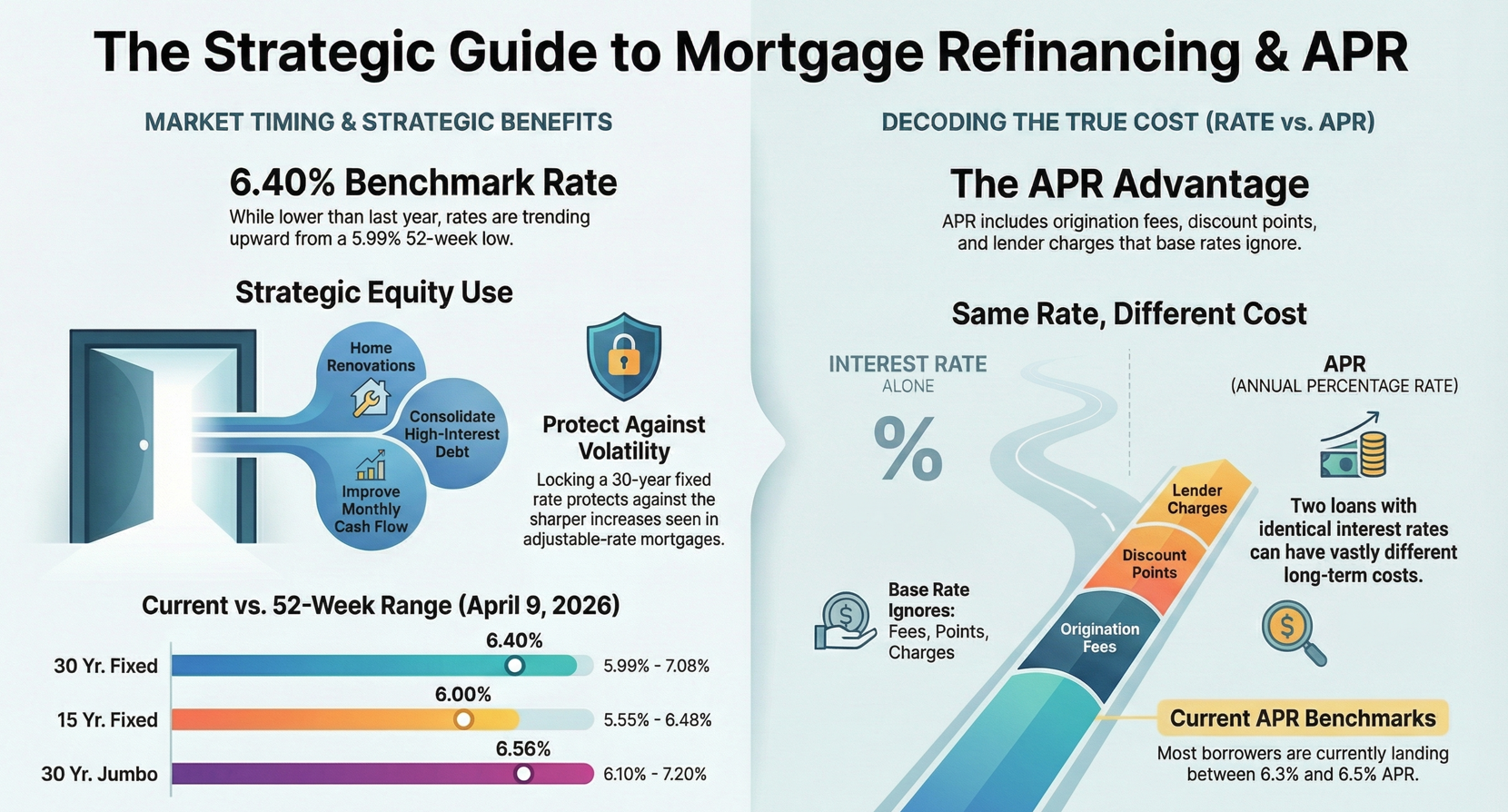

Over the past year, mortgage rates have declined across every major category. The 30-year fixed rate, which peaked above 7%, is now around 6.29%. That shift can translate into meaningful monthly savings and a substantial reduction in long-term interest costs.

But here’s where it gets even more compelling:

Depending on your financial profile, you may qualify for a rate below current market averages.

Through lender partnerships, pricing advantages, and strategic structuring—whether through insured options, shorter terms, or borrower-specific programs—I can often position clients for rates that outperform what’s publicly advertised.

At the same time, home values remain higher than they were a year ago. Even with recent cooling, most homeowners still have solid equity—giving you flexibility to refinance or access cash.

What does that mean for you? It means options:

Lower your monthly payment—potentially more than expected

Consolidate high-interest debt into a simpler, lower-cost solution

Access equity for renovations that increase your home’s value

Put your equity to work through smart investment opportunities

This is a true “sweet spot”:

Rates are down. Equity is intact. And with the right approach, your outcome could be even better than the headlines suggest.

But timing matters.

If rates move back up—or home values soften further—this window could narrow.

The bottom line:

There’s a strong chance you can improve your financial position right now—and possibly secure a better rate than you think.

Let’s take a look at your numbers and see what’s possible.

Your Mortgage Could Be Working Against You

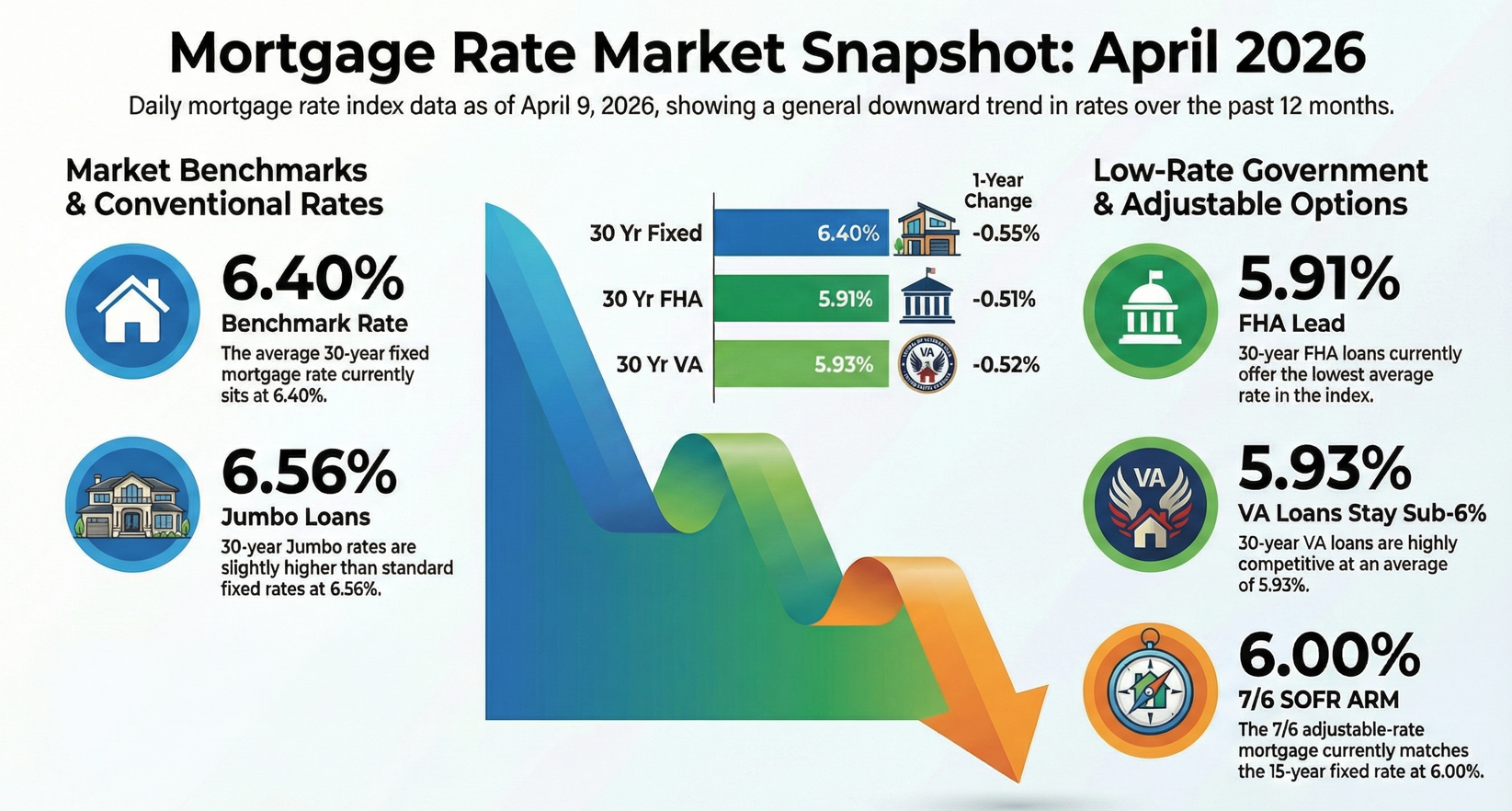

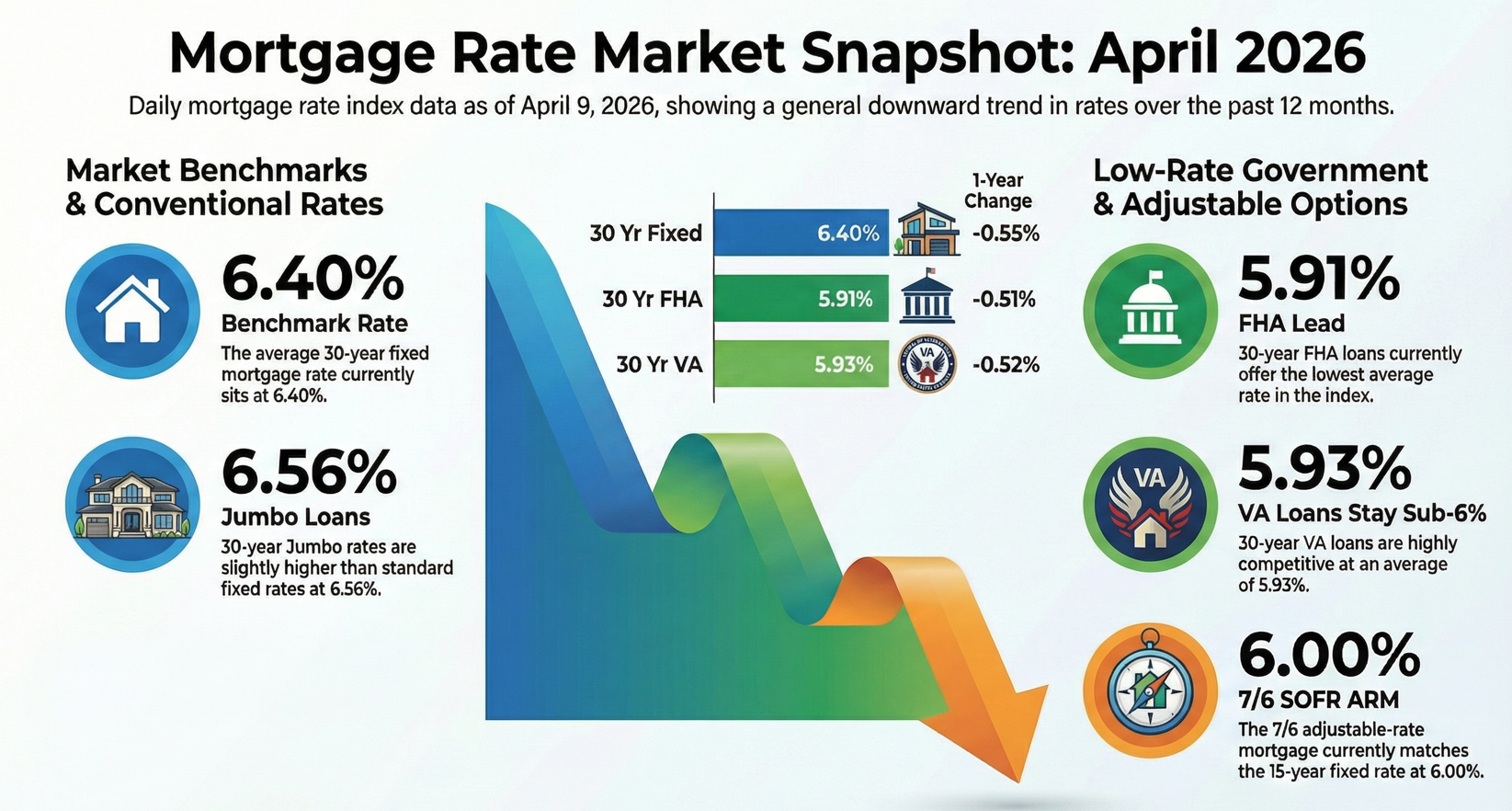

With 30-year fixed rates currently around 6.40%—down from last year but beginning to trend upward—now is an ideal time to consider refinancing. Locking in a stable rate today can protect you from market volatility, especially as adjustable-rate mortgages continue to see sharper increases. But refinancing isn’t just about securing a rate; it can also be a strategic financial tool. You can tap into your home’s equity to fund renovations that may boost your property’s value, consolidate higher-interest debt into a single lower monthly payment, or even extend your loan term to reduce monthly expenses and improve cash flow.

However, it’s important not to be fooled by a seemingly low interest rate. While the rate determines your monthly principal and interest, it doesn’t reflect the full cost of the loan, including origination fees, discount points, and other lender charges. Two loans with the same interest rate can have very different APRs—and very different long-term costs. By focusing on the APR, you see the true cost of the loan, enabling smarter comparisons, avoiding hidden fees, and choosing the option that actually saves you money. Refinancing at the right time, with a clear understanding of both your rate and APR, is a powerful way to strengthen your financial position and gain confidence in your mortgage decisions.

📞 Let’s talk about your options and see how much you could save.

Mortgage Pros is the #1 highest-rated mortgage broker, with a 4.9★ rating and 4,000+ verified reviews (most lenders average around 3★).

Check out our reviews: https://search.google.com/local/reviews?placeid=ChIJ7fFcHF3HJIgRKCOZ2Yrp3fM

The Strategic Advantages of Mortgage Refinancing in Volatile Markets

Why Refinancing Your Mortgage Today Might Actually Be a Winning Move

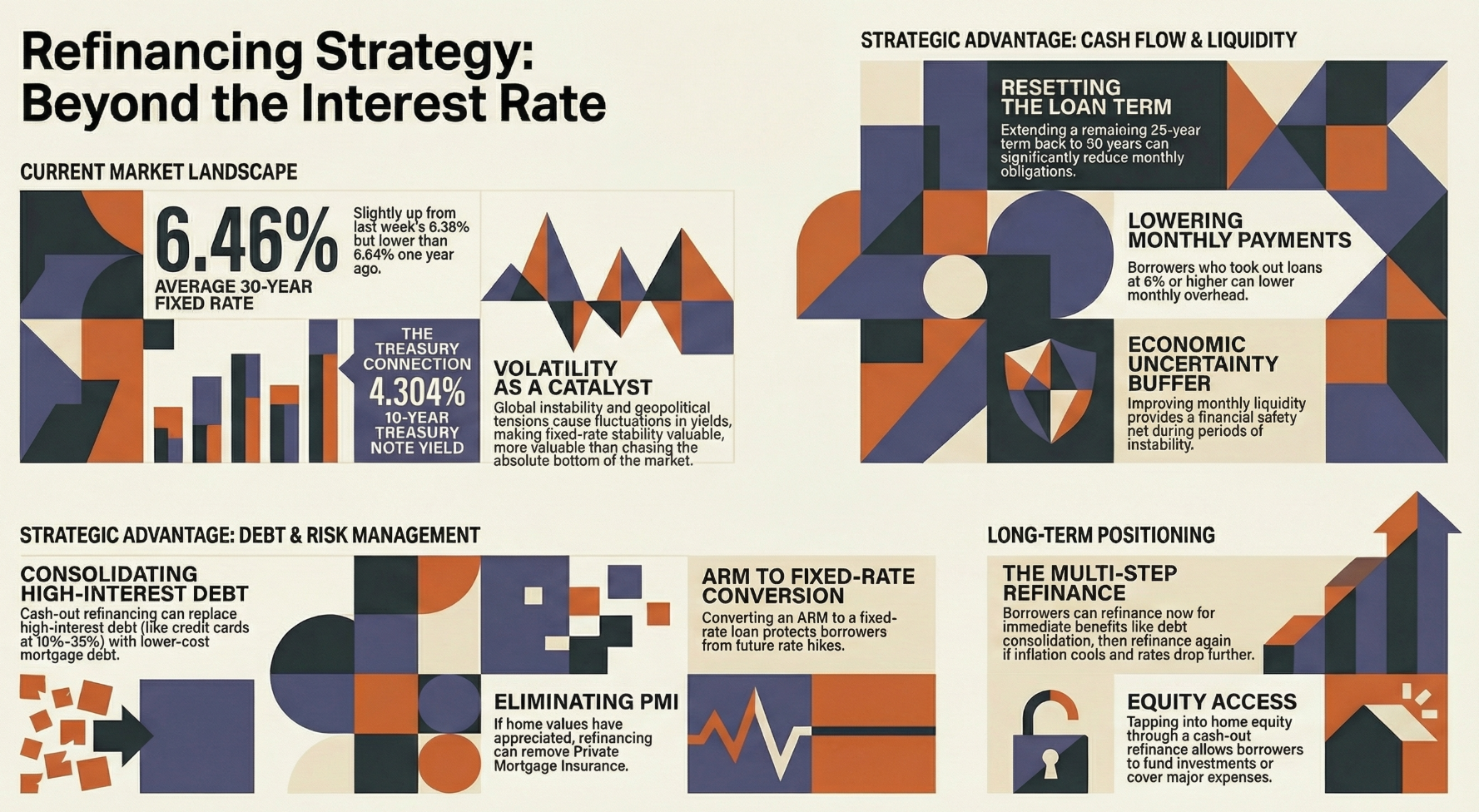

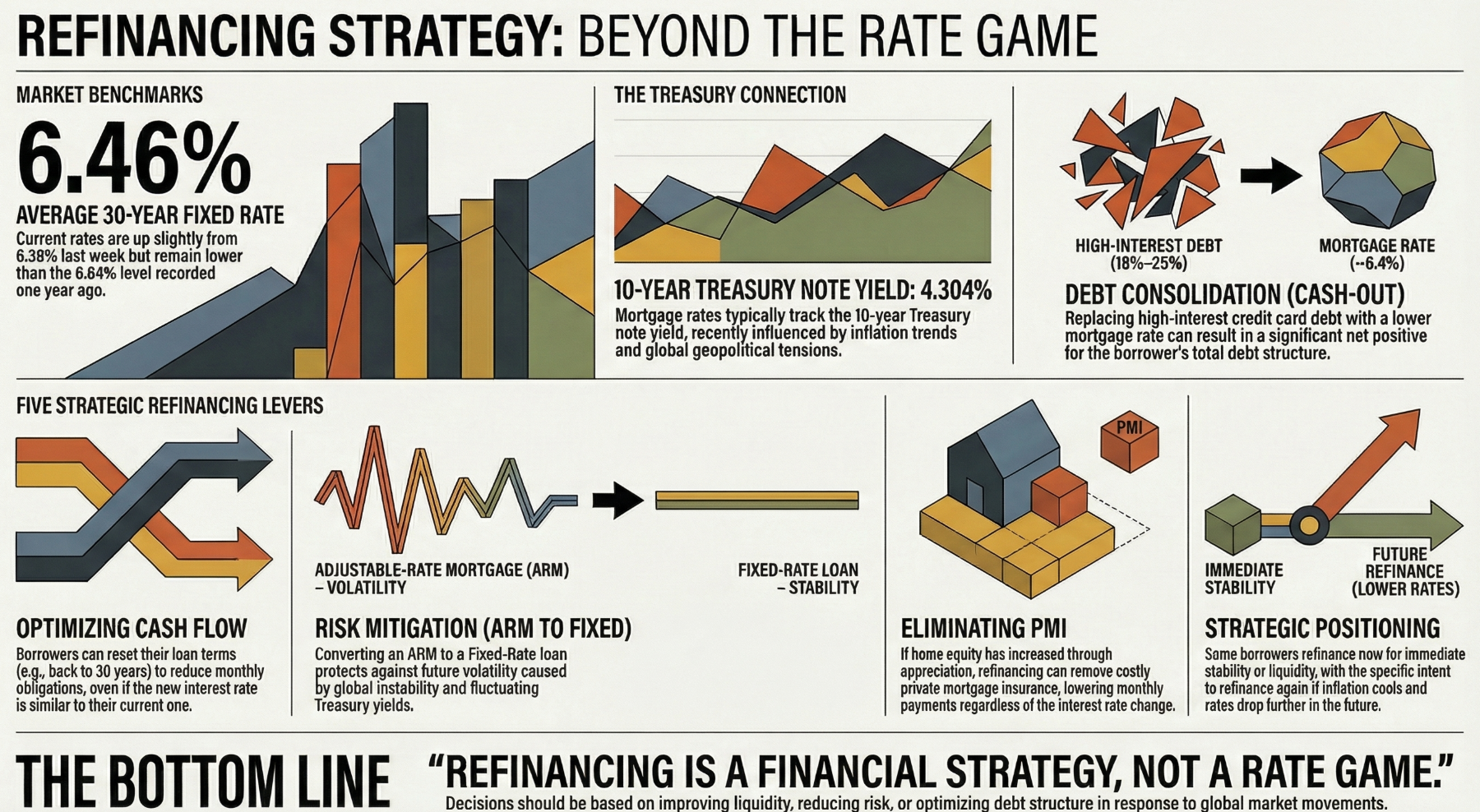

The headline numbers look like a setback, but for the sophisticated borrower, they are a signal to act. Freddie Mac recently reported that the average 30-year fixed-rate mortgage has ticked up to 6.46%. To the casual observer, this upward move from last week’s 6.38% suggests a time to retreat. However, context is everything: today’s 6.46% is still a victory compared to the 6.64% we saw this time last year.

We are currently operating in a "Refinancing Paradox." While the masses wait for the impossible return of 3% rates, the strategic homeowner recognizes that your mortgage is not a static burden—it is a fluid, sophisticated tool for managing liquidity and mitigating risk. In this environment, refinancing is no longer about "chasing the lowest rate"; it is your primary financial shock absorber against a tightening economy.

The Cash Flow Offensive: Resetting the Clock

In a world of economic uncertainty, your greatest asset isn’t just your home—it’s your liquidity. Refinancing serves as a mechanism to restructure your household’s monthly obligations by resetting your loan term. By moving from 25 years remaining back to a fresh 30-year term, you aren’t just extending a debt; you are lowering your immediate monthly overhead.

Cash flow is king. When the world is volatile, a lower monthly bill beats a lower interest rate every time.

This is a critical defensive maneuver. During periods of geopolitical tension, having extra cash on hand provides a necessary safety net. The tactical advantage of having several hundred extra dollars in your pocket every month far outweighs the theoretical "cost" of a slightly higher interest rate over the life of the loan.

Arbitraging Your Way Out of Credit Card Hell

Your home is more than a roof over your head; it is a low-interest credit line that you should be using to optimize your entire balance sheet. We are currently seeing a massive spread between mortgage rates and consumer debt. While a "cash-out" refinance might land at roughly 6.5%, the cost of carrying high-interest credit card debt is a staggering 18% to 25%.

Replacing unsecured, high-cost debt with mortgage debt is a net positive move for your total net worth. You are essentially using your home equity to "buy back" your own debt at a fraction of the cost. As the market reflects:

"Refinancing isn’t just a 'rate game.' In a market influenced by global events and Treasury yield movements, it becomes more of a financial strategy decision."

Locking the Hatch Against Global Volatility

The conflict in the Middle East and ongoing tensions involving Iran have turned the 10-year Treasury yield into a rollercoaster. Because mortgage rates track these yields, anyone currently holding an Adjustable-Rate Mortgage (ARM) is essentially gambling with their largest monthly expense.

Waiting for the "perfect" rate is a dangerous game when global instability can cause yields to spike overnight. Converting from an ARM to a fixed-rate loan now provides a definitive ceiling on your housing costs. Securing a fixed rate today is an act of proactive risk management, protecting your family from future spikes that could be triggered by the next headline out of the Treasury or the Persian Gulf.

Killing PMI with Historic Equity

We have just lived through a period of historic home appreciation. For many borrowers, this surge in equity has created a mathematical "no-brainer": the elimination of Private Mortgage Insurance (PMI).

If your home’s value has climbed enough to put you past the 20% equity mark, refinancing to remove PMI can result in a lower total monthly payment even if the interest rate itself stays flat or increases slightly. When you stop paying an insurance premium that only protects the lender, you effectively give yourself a permanent monthly raise.

The Bridge Strategy: Playing for the Next Drop

The most sophisticated move a borrower can make right now is the "Bridge Strategy." This involves the audacity to refinance today for immediate benefits—like debt consolidation or cash flow—with the explicit intent to refinance again the moment the market shifts.

Refinancing today is a tactical maneuver to survive and optimize the current market while staying "option-rich." If inflation cools and the 10-year Treasury yield continues its descent, you will be in a prime position to strike again. This is a proactive financial stance: you secure your stability now, using today’s rate as a bridge to future opportunities.

Conclusion: Beyond the Interest Rate

Refinancing is ultimately a tool for optimizing debt structure and insulating yourself from risk. While the 10-year Treasury yield currently sits at 4.304%, it is merely a marker on the map, not the destination. By looking beyond the headline interest rate, you can make decisions that prioritize liquidity, stability, and long-term wealth.

The real question isn't whether the rate is 6.46% or 6.38%. The question is: are you viewing your mortgage as a passive monthly bill, or as the strategic anchor of your total financial health?